‘Price is what you pay. Value is what you get’

‘Be fearful when others are greedy and greedy when others are fearful’

Warren Buffet

More than €615bn (transactions with disclosed values) were spent on 1780 M&A transactions over the last decade by the 55 world largest FMCG companies. Most of those transactions failed to deliver ROI. Worse, the companies that spent the most on M&A destroyed the most shareholder value. Why?

We reviewed all those 1780 transactions leveraging PitchBook database. We crossed that data with the 2012-22 Euromonitor sell-out data by brand/ countries (>100k+ combinations) and the last 10 years financial reports of the world largest FMCG companies. We then asked ourselves the following questions:

- What has been the role of M&A in the overall FMCG industry growth & in shareholder value creation?

- Who have been the greatest M&A Winners & Losers and why?

- What have in common the most successful M&A transactions & the most successful acquirers in the FMCG industry?

- How M&A activity has evolved within the FMCG industry & within each vertical (Food & Beverage, Beauty Personal Care, Consumer HealthCare, PetCare, Household) and why?

If there is no universal truth and our approach has some limitations (~30% of transactions have undisclosed value for example, some acquired brands are still too small in 2022 to appear on Euromonitor tracking), clear learnings emerge.

Here is our perspective:

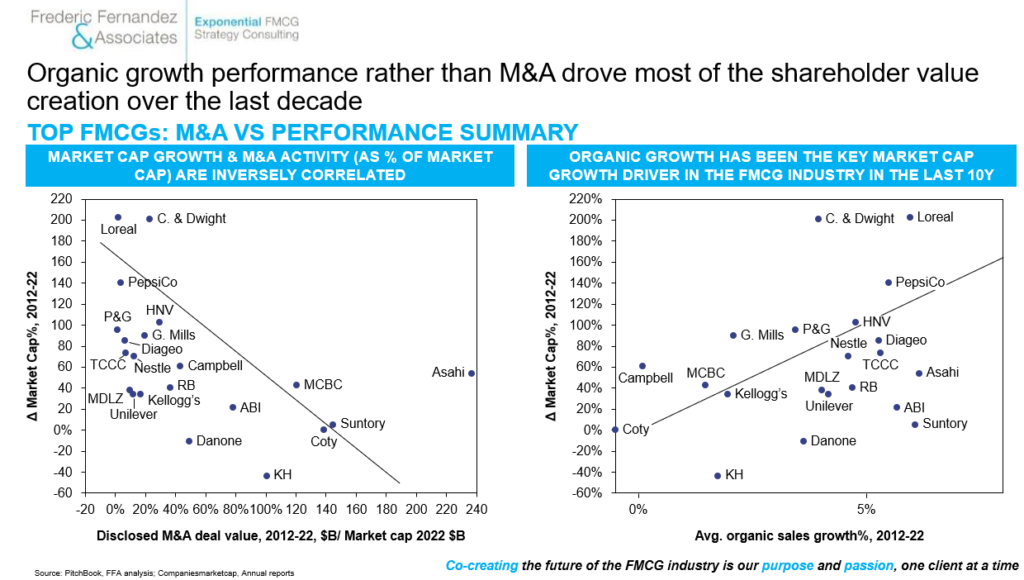

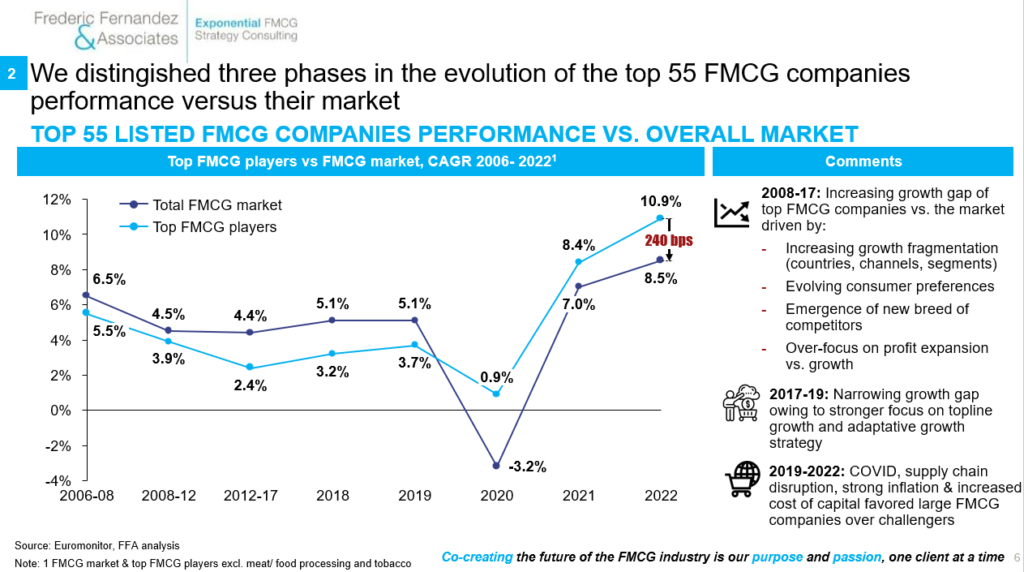

1) Organic growth performance, and not M&A, has been the key driver for shareholder value creation over the last decade in the FMCG industry. Companies that prioritized organic growth while engaging into frequent mid-size (€0.5-6bn) M&A transactions (L’Oreal, Church & Dwight, PepsiCo, Heineken…) outperformed their peers, especially the ones that pursued the largest transactions (>€10bn: ABI, Kraft-Heinz, Danone, Coty…) that ended up performing the worst

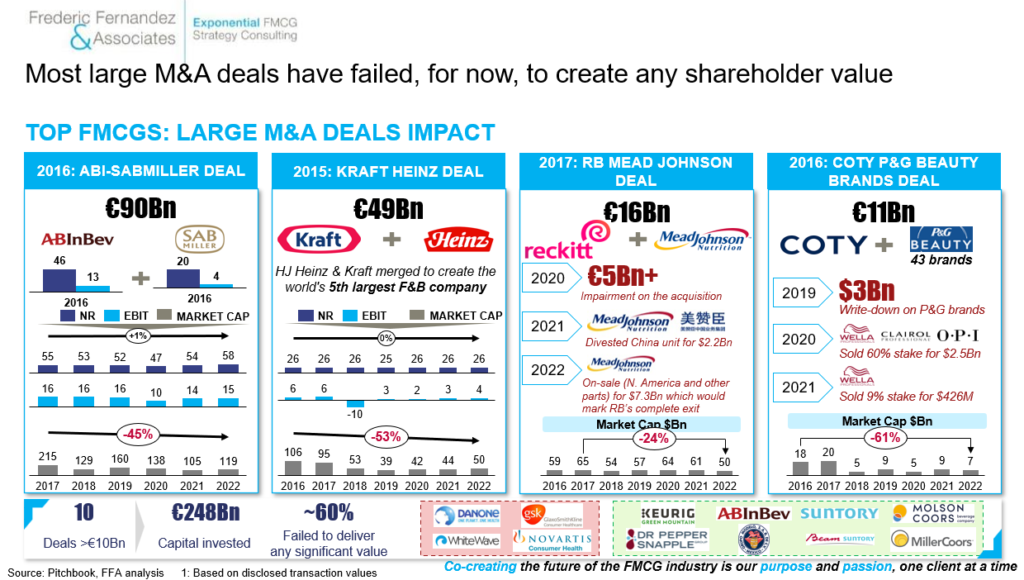

2) Most large deals have, for now, failed to deliver shareholder value. Far the contrary

Few thoughts:

- First a caveat here, M&A transactions need to be assessed holistically & short-term financial metrics are important but are only one lens and the stock market does not necessarily have the monopoly of the truth, especially over the long-term

- Second, we have a mixed bag in those five transactions. Some are great assets that suffered from somewhat poor execution (SAB-Miller, the divested P&G brands to Coty – think Cover Girl) and some were more challenging assets (when a majority of Mead-Johnson revenue sits in China and birth rate is structurally declining there, it is a uphill battle)

- Third, it is hard to capture long-term indirect value & strategic optionalities that could be enabled by those deals:

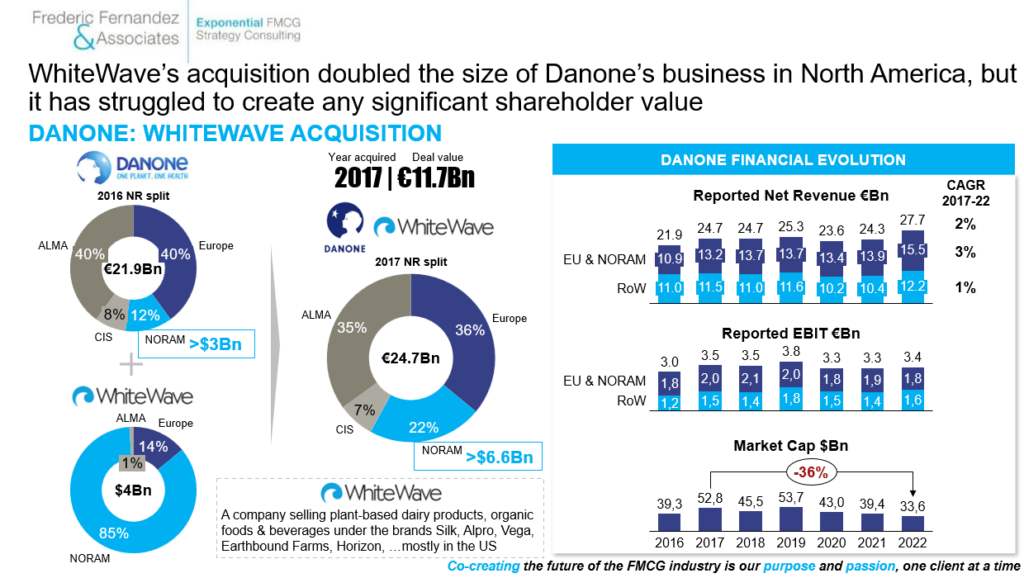

i) If in 10 years, Danone outperforms thanks to its edge on plant-based, will the WW deal be quoted as a ‘decisive accelerator’?

ii) For ABI, what would have been the cost & the time required to build similar positions as SAB-Miller in Africa, especially after risk-adjustment? Anyone that understand the capital intensity behind beer brewing & distribution and the upfront investments required to build a brand in a highly fragmented retail & media environment know that it is a very hard thing to do. Then, look at the demongraphic potential of Africa over the next 50 years. Finally, what if in 10 years BEES (the ABI EB2B platform) ends up being a $100bn market cap listed stand-alone entity and that 50% of its value is driven by Africa? Will we call this then a genius move?

- Having said that, things could have been better managed with those large transactions and especially on the ABI & Coty ones:

i) First, the focus was maybe too much on the Target’s profitability improvement vs. topline growth acceleration

ii) Second, the acquirers did not have necessarily enough organizational bandwidth to execute a seamless integration without impacting the acquirers’ base business

iii) Third, financial markets expectations could have been better managed through highlighting better the huge complexity behind such integrations, the cost of building vs. acquiring and the associated long-term benefits/ optionalities

We have to recognize that in hindsight, it is always easier to comment. The French dramatist Destouches used to write ‘Criticism is easy, and art is difficult’. Indeed

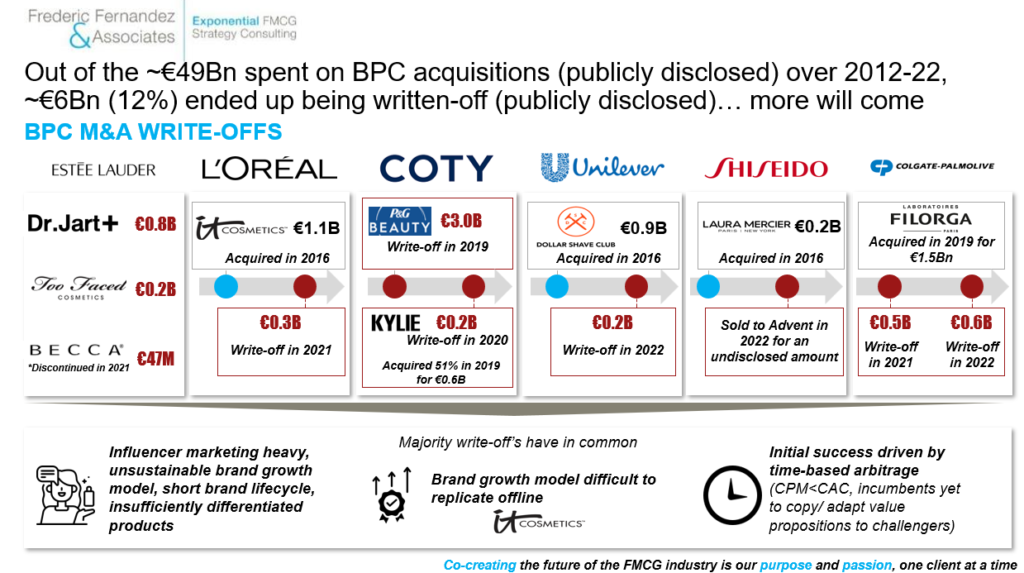

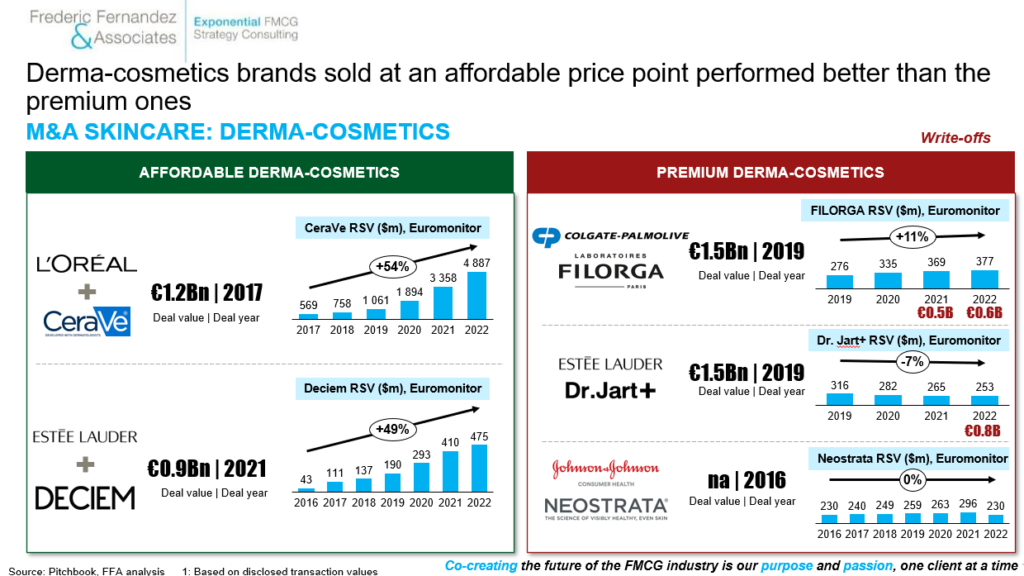

3) Out of the €49bn invested on Beauty Personal Care (BPC) acquisitions over the last decade, 12% (for now) ended up being publicly written-downs (12% of the total invested) and more will come

If those impairments are unevenly distributed (Coty, Estee Lauder, Colgate being more impacted than L’Oreal), there is a trend. Here also, we have a mixed bag of reasons that differ from one asset to another:

i) Many digital-first Color Cosmetics brands were dependent on the founders & social media to recruit consumers. Their products were insufficiently differentiated and they went through a brutal hype/ de-hype cycle

ii) Some brand growth models, like IT Cosmetics that was mostly QVC driven in the US, were not easily transferrable to a retail environment

iii) Some businesses like Dollar Shave Club had an unsustainable CAC-CLTV equation with the continuous rising CPM, the emergence of online competitors (incl. Gillette), a narrowing price advantage following the price increase on their offering post Unilever acquisition and Gillette price decreases on their blades

iv) Regarding the Filorga/ Colgate deal, the size of the impairment (€1.1bn out of a €1.5bn acquisition) and the speed at which it took place (within 36 months post acquisition) suggests a large problem that may go much beyond travel retail & China COVID-induced disruption. Our hypotheses are that Filorga brand growth model may not be performing in pharmacies as well as it should (no channel exclusivity, also sold in prestige beauty channels; potentially too ‘mass’ marketing mix – TV advertising, outdoor…) and that Colgate did not have necessarily the international scale-up capabilities on the pharmacy & prestige beauty channel to accelerate dramatically Filorga growth. Only our humble hypotheses

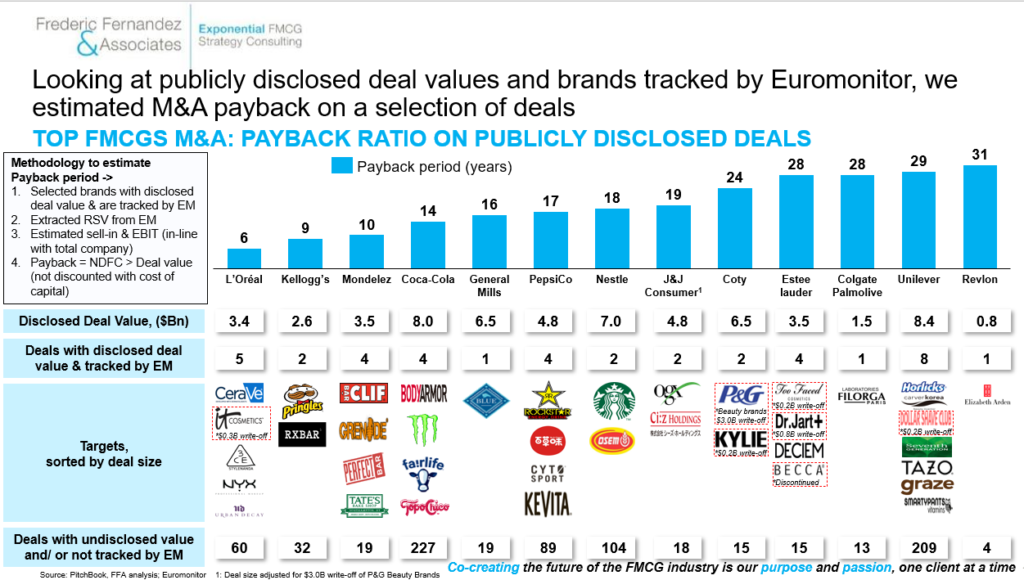

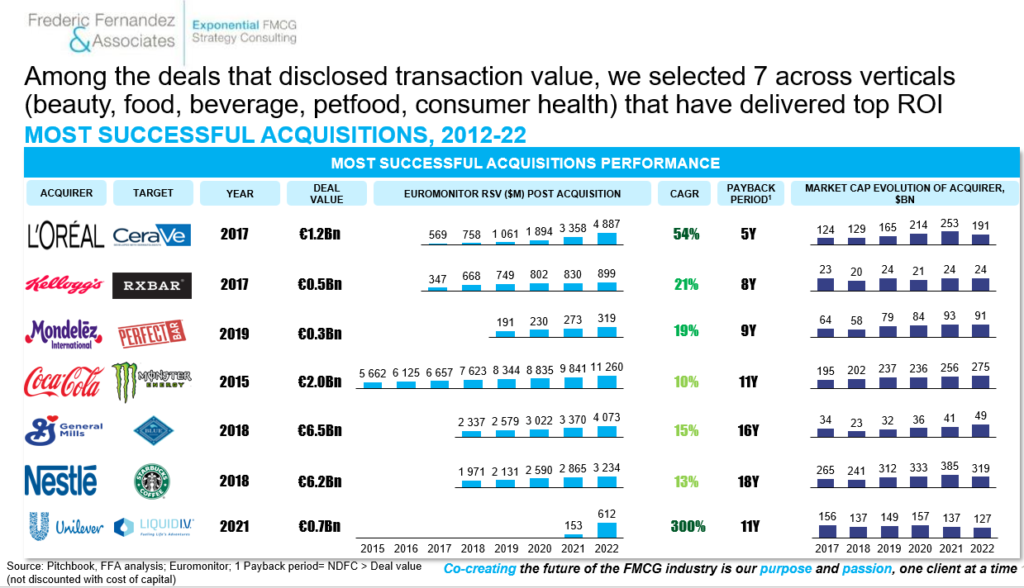

4) Our research on a small sample of deals (publicly available deal value AND brands tracked by EUROMONITOR) indicates a large standard deviation in M&A ROI performance among the world largest FMCG companies. Mid-size deals (€0.5-6bn value) outperformed. High ROI deals took place across most verticals (Household is the exception)

Most of those high ROI deals (CeraVe/ Starbucks/ RXBAR/ Monster) have in common four critical factors:

- Being on a sub-segment growing much faster than the vertical in which they operate (affordable dermo-grade skin care, coffee, snack bar, pet food)

- A Target with a fit-for-purpose brand growth model/ 4Ps

- An asset that reached enough maturity, size & strength to be scaled-up (which often translates into a mid-size revenue bracket of €100-500m and a valuation bracket of €0.5-6bn)

- An acquirer with the capabilities to execute efficiently (right expertise, critical mass on the right distribution channels globally, strong M&A track records)

Beyond the above, General Mills really impressed us by its ability to get into Pet Food (which was a white space for them) with Blue Buffalo and sustain a superior growth rate. Few FMCG companies have been able to make ‘Adjacent’ moves a success

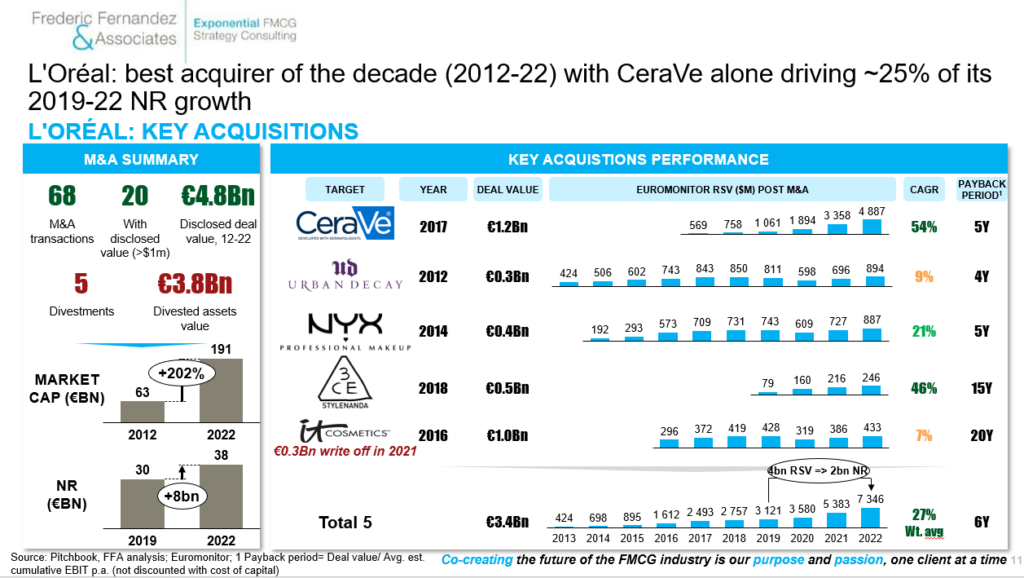

5) L’Oreal emerged as the winner of the last decade. Its star acquisition, CeraVe, drove alone 25% of its growth over 2019-22. L’Oreal continues its long tradition of successful M&A in the Beauty space. Out of its 36 international brands, only one was not acquired: L’Oreal Paris

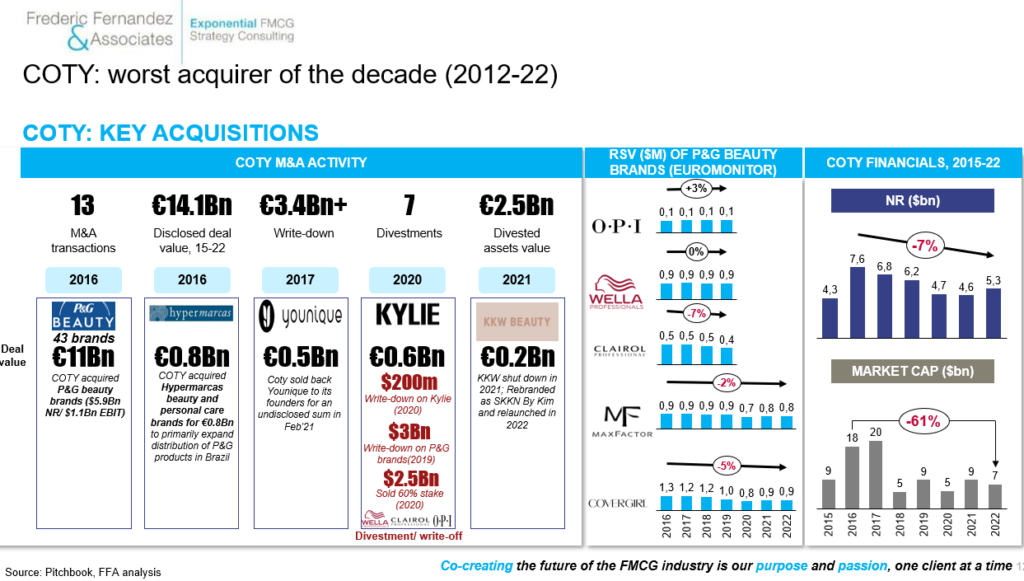

6) Coty emerged as the worst acquirer of the last decade (P&G Beauty brands, Younique, Kylie): it is the story of a $9bn market cap beauty company that spent >$15bn in M&A and that ends up being a $7bn cap in 2022 (they divested some of those assets for $2.5bn in 2020). The story is not over though as Coty has embarked into a turnaround since 2020 with the appointment of its new CEO, Sue Y. Nabi, and early results are promising

7) Skin Care M&A that focused on affordable derma-cosmetic value propositions performed best. Investments on high price-point derma-cosmetics have failed for now to deliver shareholder value, worse most recorded significant impairments (Filorga, Dr.Jart+)

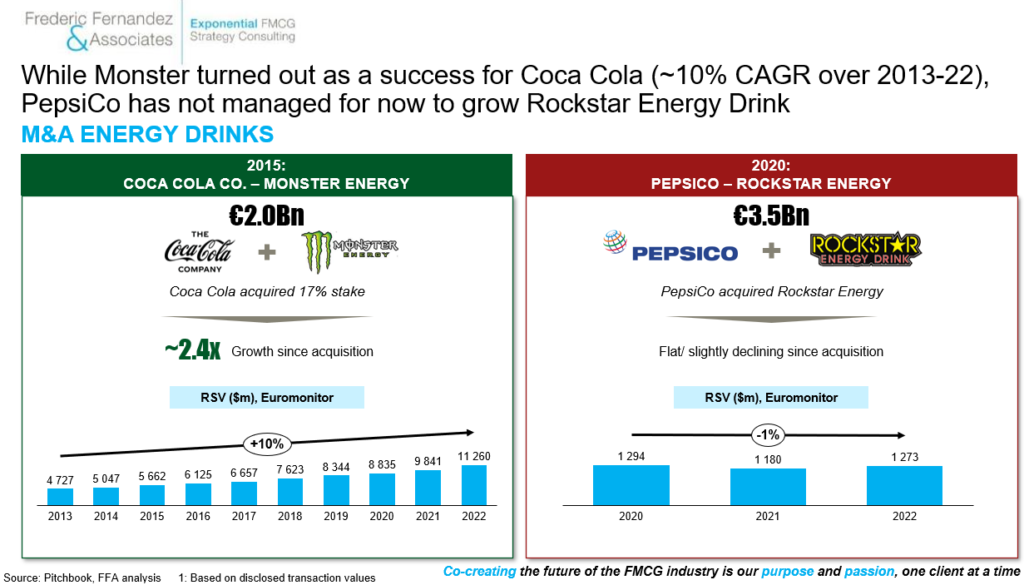

8) Not all Energy Drinks transactions have, for now, delivered results

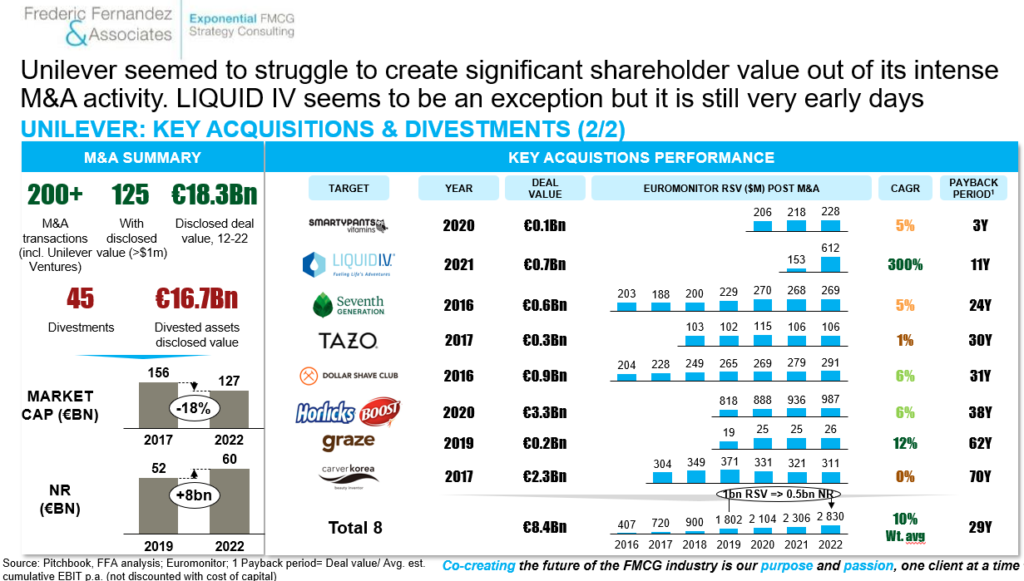

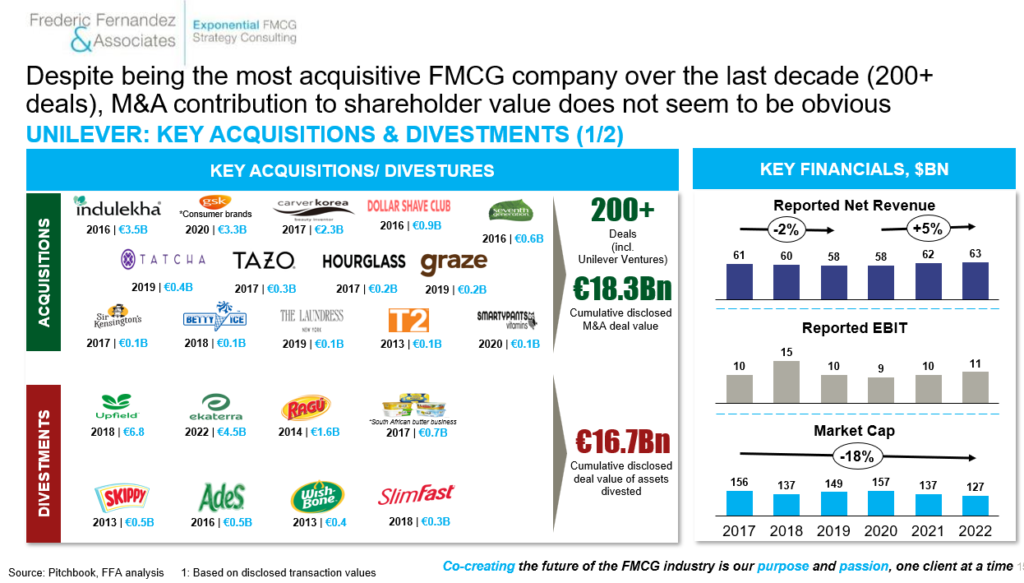

9) Unilever: despite an intense M&A/ divesture activity (especially on small deals – 75), its M&A contribution to shareholder value has not been obvious. LIQUID IV is a stand-out although it is still very early days

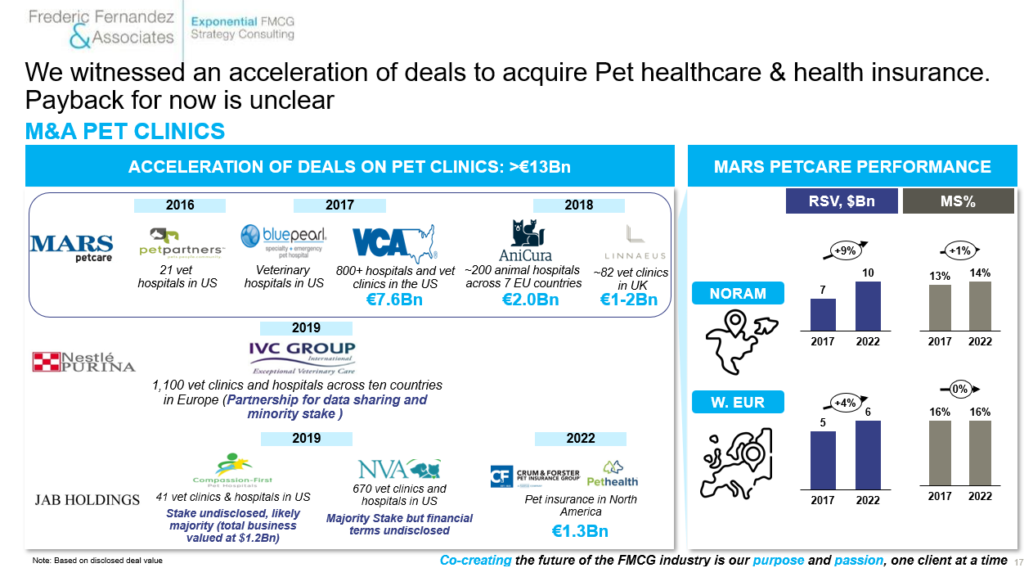

10) ROI on Pet Clinics acquisition remains for now difficult to assess. It was one of the big bet of Mars PetCare with more than €10bn invested

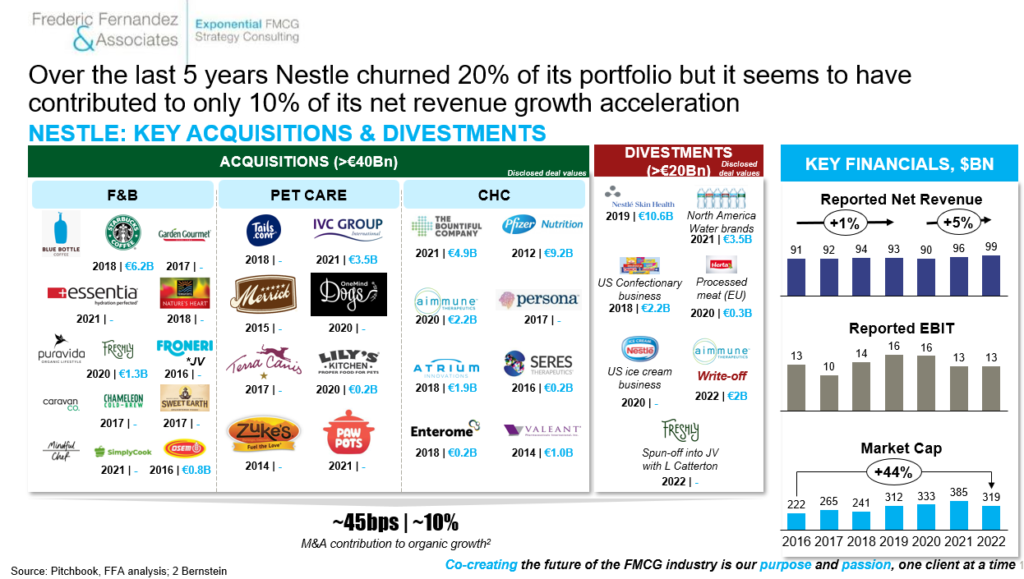

11) If Nestle completed a large portfolio transformation (20% rotation since 2017) through M&A/ divesture and if shareholder value creation has been top-tier over the last 5 years, those results seem to have been more driven by organic growth performance than through M&A/ divesture as contribution of the latter to organic growth has been limited (estimated at ~10% – let’s keep in mind it is a $99bn company). Like the best acquirers (including L’Oreal with IT Cosmetics), Nestle had some missteps along the way (Aimmune, Freshly) but acted decisively (in the process to put them back on sales)

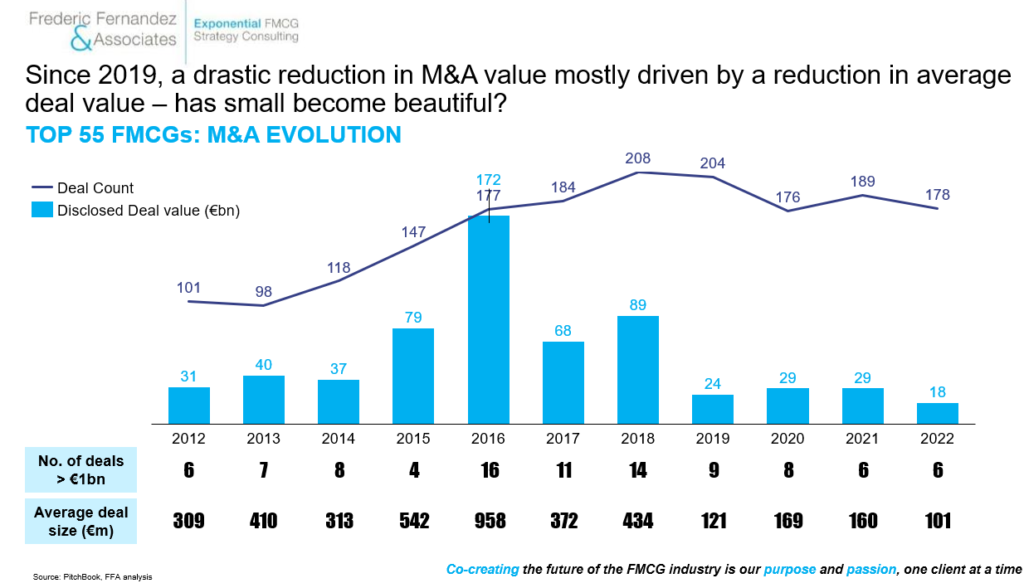

12) Looking at macro M&A trend in the FMCG industry: since 2019, we witness a drastic reduction in M&A value mostly driven by a reduction in average deal value – small has somewhat become beautiful

Few comments on the above evolution & one watch-out:

- M&A value increased over 2015-18 under the impulsion of few large players that completed few mega-deals (mostly 3G co-owned companies like AB-Inbev & Kraft-Heinz or JAB co-owned like Reckitt, Keurig-Dr Pepper, Coty) mostly (but not exclusively) driven by the intent to consolidate verticals & increase profitability

- From 2017/18, we witnessed the rise of pro-growth strategy often leveraging M&A, mostly focusing on medium size challenger brands with an attempt to close the increasing growth gap between the world largest FMCG companies and the rest of the market

- From 2019, we witnessed a sharp reduction in M&A value driven by a drastic reduction in average value per transaction. This change has multiple reasons:

i) The 2020-22 period called for more financial prudence and saw a reduction in the execution & financial bandwidth of many companies that ended up being very busy managing multiple crisis (COVID related disruptions, Supply, Ukraine War, Inflation…)

ii) Assets prices remained elevated/ inflated vs. fundamentals and detered many acquirers

iii) Organic growth came easier for the top FMCG companies in a context challenger brands were more penalized than large brands (retailer driver SKU reduction, COGS inflation, supply chain disruption, increase in cost of capital)

iv) The world largest FMCG companies started to integrate some of their recent M&A learnings (majority of large transactions failed, many mid-size deals were written-down) and doubled-down on small acquisitions with the intent to spread risks

If small deals have a role to play in a M&A strategy, alone they tend to deliver a lower ROI than mid-sized transactions and are often not enough to move the needle.

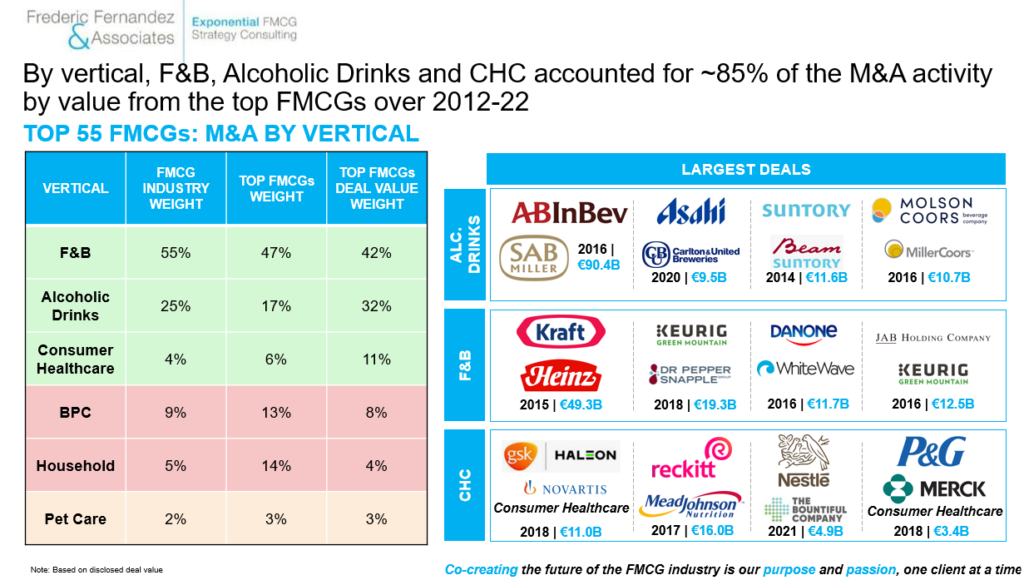

13) Food & Beverage, Alcoholic Drinks & Consumer Health verticals have been the most active verticals

- Beverage & Alcoholic Drinks in particular are the verticals where economies of scale are the most important (capital intensity on manufacturing & distribution) and where consumer preferences evolved most, explaining this intense M&A activity

- Consumer Health Care (CHC) M&A benefited from the Big Pharma intent to spin-off their CHC businesses and from incumbents intent to accelerate in a what has been a growth/ profit accretive area (Reckitt, Nestle, P&G, UL) vs. HPC/ F&B

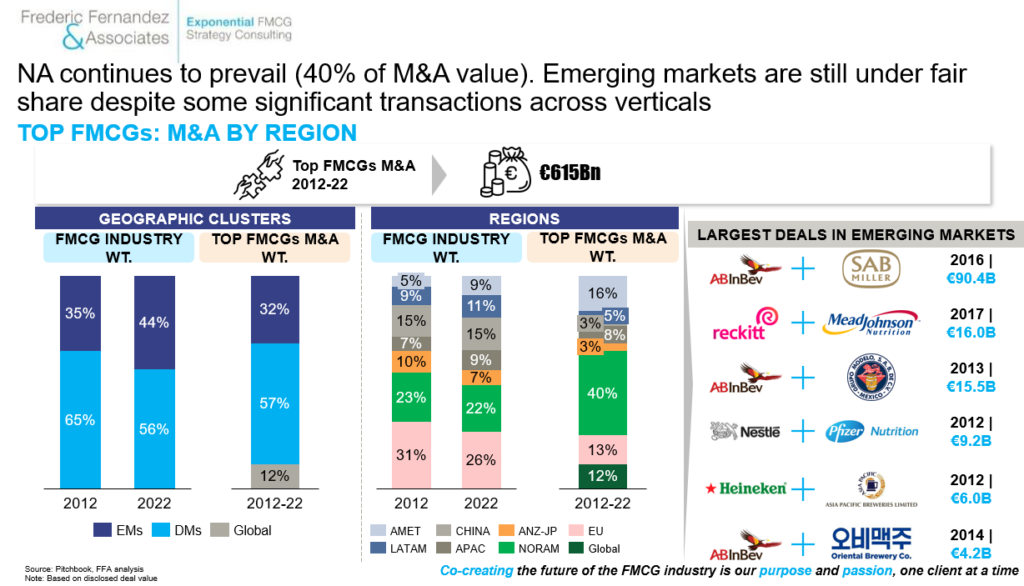

14) North America remained the favourite ground for M&A (40% of M&A deal value). Emerging Markets is the region the most under fair-share despite few major transactions mostly initiated on beer & CHC

- North America (NA) remained the favourite ground for M&A (40% deal value vs. 22% weight of the FMCG industry) for multiple reasons:

i) NA market size provides a unique ground for local assets to scale-up

ii) NA market is seen (sometimes wrongly) as a good predictor for future global success

- Emerging Markets received comparatively less investments (because of a higher fragmentation/ lower scale-up potential, higher risk) although many large transactions took place in EMs (or had sizeable assets in EMs) – e.g. ABI-SAB Miller & Modelo/ Heineken-APB/ Reckitt-MJ/ Nestle-Pfizer Nutrition

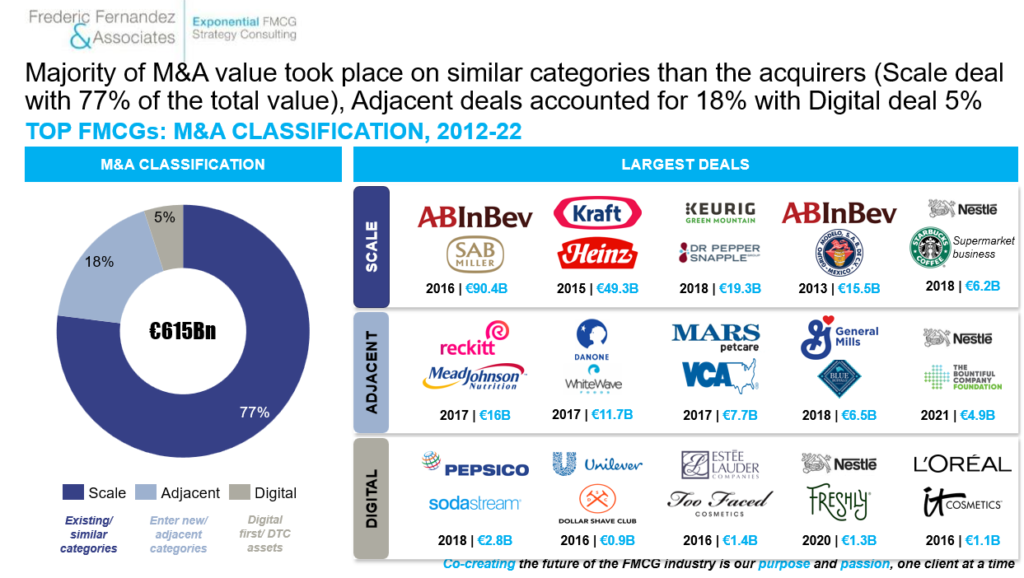

15) Most of M&A investments (77%) were directed on existing categories with the objective to leverage acquirers’ scale. The Pet Care vertical was an exception with its foray into pet clinics

- The favourite value creation tactic of the world largest FMCG company was to leverage their expertise on existing categories & their GTM scale to create disproportionate value (77% of M&A value)

- A minority of the M&A value sat on adjacencies (18% – Reckitt/ MJ, Danone/ WW, GenMills/ Blue) and digital/ DTC-first assets (5%)

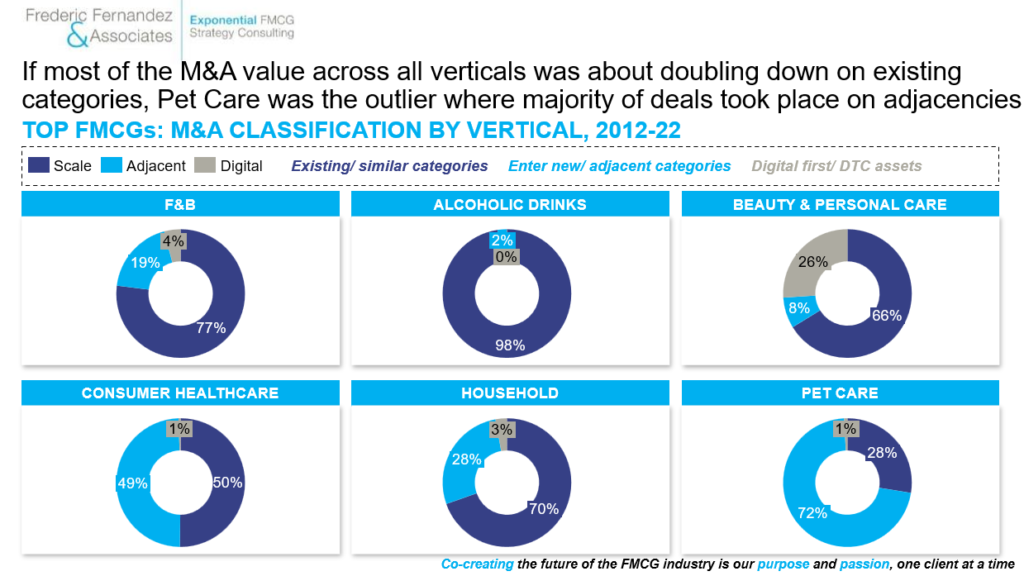

PetCare was interestingly the vertical that saw the most investments going into Adjacencies (72% of M&A value) than any others, mostly because of the rush to acquire vet clinics over 2017-19

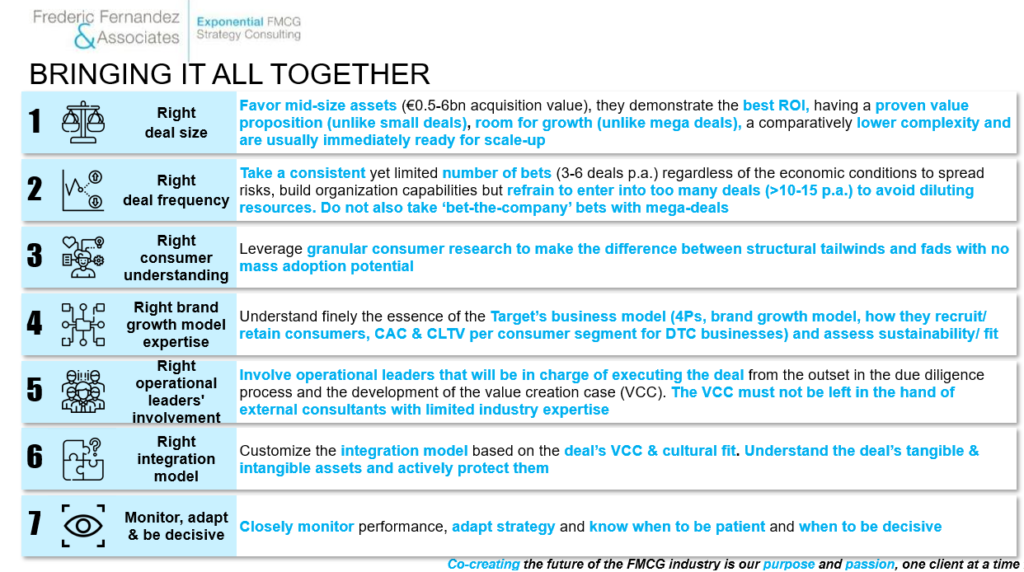

Bringing it all together & breaking the code of successful M&A in the FMCG industry – 7 key learnings emerge:

1) Size matters:

- Favor mid-size assets (€0.5-6bn acquisition value), they demonstrate the best ROI despite their high price tag that can deter many. An asset that has scaled up to >€100m revenue has demonstrated sustainability/ strength in its brand growth model & is often ready for scale-up. ‘Price is what you pay & value is what you get’ (Buffet). Understand the difference between both

- Smaller assets (<€100m revenue) may still be unproven for global expansion & over-dependent on their founders implications. At such, their risk adjusted profile are often much riskier than mid-size transactions. We are yet to see a case of a FMCG company being successful at acquiring a high number of small assets and scaling them up successfully

- Mega deal (>€10bn) are the riskiest (one transaction, often already scaled-up & well optimized assets and most destroyed shareholder value over the last decade). At such, they should be handled with extreme prudence (focus on BOTH topline growth & costs synergies, integrate the cost of integrating & the cost of not doing in the business case & acquisition story, manage carefully expectations with the financial community)

2) Frequency matters, irrespective of ‘weather’:

- Top performing acquirers acquire 3-6 mid-size assets per year. They take bets ‘all-along’, they do not take one single large ‘bet-the-company’ bet. This way, they minimizes risk and maximize value creation case (ie. scale-up potential). They also build knowledge & develop M&A organization capabilities across the M&A cycle (assessment, deal-making, integration, value creation case delivery)

- Top performing acquirers shop in all weather (L’Oreal completed its largest ever acquisition in Q1 2023 – $2.5bn – with Aesop). ‘Be fearful when others are greedy and greedy when others are fearful’ (Buffet)

- Beware of too many small acquisitions per year (>10-15), risk is high to drain organization resources (even if those are executed within a Corporate Venture Capital Fund) & to end up with a ‘house of dogs’ (a myriad of small assets requiring high attention but with low scale-up potential). Unilever?

3) Deep consumer understanding matters & helps to make the difference between structural tailwind & fads:

- Energy drink is a long-term trend with mass penetration potential. Probiotic soft drink, much less so

- Affordable dermatologist-grade skin care is a long term trend with mass penetration potential. The latest influencer color cosmetic brand with a masstige pricing, much less so

- Too many FMCG companies neglect granular consumer research in their due diligences phase

- It is critical to understand clearly the Target’s Brand Growth Model: ie. who are the Target’s consumers, what are their drivers/ barriers/ triggers/ occasions/ 4Ps preferences, what is the brand’s performance across Zero-First-Second Moment Of Truth and how do they recruit/ retain consumers

- For example, many insurgent brands (on F&B but also on BPC) in the US have failed to break the $100m revenue ceiling. Reason is that they have niche adoption potential. So even if those brands get maxed out on distribution, they will rotate poorly. Understanding penetration/ frequency/ basket potential of a Target is critical

4) Understanding the essence of your Target’s business model matters:

- Know what you know and most importantly what you don’t know and surround yourself accordingly

- Too many acquisitions fail because of insufficient expertise on the Target’s category and/ or on its brand growth model. Assessing a premium dermo-cosmetic business that usually relies on Health Care Professional (HCP) marketing & pharmacy channel exclusivity/ trust is different than assessing a personal care business that relies on mass distribution & TV advertising. Mixing both may not be optimal (cf. the Filorga case, €1.1bn write-off, ie. 2/3 of the acquisition price)

- DTC business are intrinsically different than legacy FMCG businesses: few have a sustainable ‘ownable’ value proposition vs. alternatives and most have been subsidized by cheap CPM & capital with a negative real interest rate. Being able to understand CAC & CLTV & des-average them per consumer segment to craft a profitable growth strategy is critical

- Failing to understand those realities have led invariably to (large) write-downs

5) Involving your operational leaders in due diligences & in the elaboration of the value creation case matters:

- Value creation case needs to be rooted in hypotheses vetted by the leaders of the teams that will execute it

- Too many deals assessments are still completed in silos by internal M&A and external consulting teams with limited operational expertise

6) Integration model matters and depends on the value creation case & the cultural fit between the two organizations:

- There is no one size-fits-all integration model (stand-alone, semi-integrated, fully-integrated). They all have their pros & cons and need tailoring

- The right integration model depends on the value creation case (cost take-out, revenue growth through scaling existing brand growth model or through scaling up physical distribution or a mix of both…) and cultural fit

- Be very clear on the deal’s tangibles (respective organizations give & get) & intangibles (how the Target’s culture is responsible for success…) assets and ensure to protect those

7) Keep monitoring, learning and adapting & know when to be patient and when to be decisive:

- Some deals go as planned but most do not

- Monitor frequently progress, adapt strategy & execution and be patient

- Equally, know when to draw a line and cut your losses & refocus your resources on other priorities (cf. Nestle decisiveness on Aimmune & Freshly). Even the best acquirers have non-performing deals that they write-down/-off or ultimately discontinue. Don’t hang too long on your losers and move on

Let’s close this article on the two opening quotes:

‘Price is what you pay. Value is what you get’

We hope the above insights will help to better understand what are the drivers between the two in the FMCG industry

‘Be fearful when others are greedy and greedy when others are fearful’

We hope that the high failure rate of M&A in our industry will not be a deterent to leverage the increasingly favorable context to acquire assets. At the end of the day, it is in downturn that Winners make the difference & widen the gap

Exciting & decisive times.

To get all our FMCG CEO insights, please sign-up to your bi-weekly newsletter:

#fmcg #cpg #strategy #ceoinsights #mergersacquisitionsdivestitures #growth #acquisitions #venturecapital #privateequity

To follow Frederic, please click Here, To contact him, email at: frederic@fredericfernandezassociates.com

About the author:

Frederic Fernandez is a strategic advisor in the FMCG industry. He is the Managing Director and Partner of Frederic Fernandez & Associates (FFA) a global bespoke Strategy Consulting Firm exclusively focused on the FMCG industry across all key verticals (Food & Beverage, Alcoholic Drinks, Beauty & Personal Care, Household, Consumer Health Care, PetCare, Tobacco RRP). Its purpose is to co-create the future of the FMCG industry, one client at a time. The Firm helps the CEOs and the Boards of the world’s largest FMCG companies on selected areas: Growth and Profit acceleration, New Retail/ EB2B/ Ecommerce/ DTC strategies and M&A (buy-side & sell-side). The Firm’s head office is located in Zug in Switzerland. The Firm’s team intervenes all across the globe. To know more about the Firm, please visit its website: www.fredericfernandezassociates.com

No FFA employees own any stocks or financial instruments of any FMCG companies or companies mentioned in the above article. All the above information are public information